Get Started With

servzone

Overview

An NGO can be listed as a Section 8 company after the Companies Act 2013 or as a trust supporting the Trust Act 1882 or as a society under the 'Societies Act 1860'. Section 8 is a method of incorporation of an NGO under the Companies Registration 'Companies Act 2013'. Under Section 8, any company should be referred to 'art', 'science', 'commerce', 'technology', 'sports', 'education', 'social research', 'social welfare', 'religion', 'charity' Can be registered for promotion. 'And' Protection of the environment 'etc.

Latest Incorporation of Section 8 Companies as per Companies Act 2013 - Sixth Amendment 2019

MCA Consulting Companies (Incorporation) 6th Amendment Rules, 2019 dated June 7, 2019 have revised the incorporation criteria to include Section 8 companies. This rule has come into effect from August 15, 2019.

Subsequently, the new rule has made the licensing and registration process easier for Section 8 companies. Now applicants can apply for registration of Section 8 companies by filling a single application in Form SPICe. The MCA website has provided the following instructions that will clear the air of doubt:

- Pending Form INC-12 SRNs for new Companies pending on the part of respective RoCs will be considered as ‘Rejected’ on 15th August 2019. Such applicants can directly file SPICe for the purpose of receiving License Number and for forming Section 8 Companies.

- Those shareholders who already own a license number and are waiting to file the SPICe form so that they can incorporate Section 8. Companies should note that the forms will be processed once a fixed time interval is allowed for the work flow change to take effect.

- Those stakeholders who are done with filling the SPICe form, but are pending from the CRC, may have to wait for processing of these forms once the work flow changes.

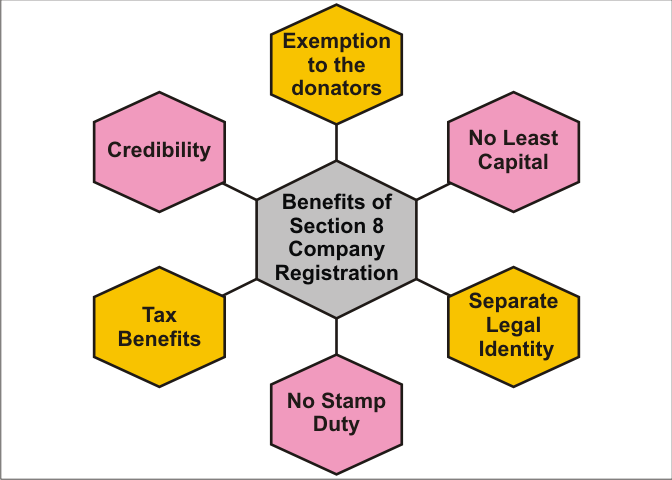

Benefits

Comparing a non-profit organization does not mean that the company cannot secure profits or commissions. This simply means that the company can earn income, but the promoters do not benefit from those benefits. There are also several tax exemptions for such companies. Even donors providing on behalf of the Section 8 company have the option of claiming tax exemption against these donations. Some of those allowances are given below:

- There is no capital

There is no minimum capital requirement for Section 8 company registration in India.

- Tax benefit

There are several tax indemnities under Section 8 company registration in India.

- No stamp duty

There is no stamp duty requirement on inclusion of a Section 8 company in India as it provides for installment of stamp duty on MOA and AOA of private limited business.

- Separate Legal Identity

Section 8 is a separate legal entity of company certification. It takes a different legal personality from its feet and arms.

- Credibility

Section 8 company has more credibility than any other form of a philanthropic / charitable organization.

- Donation to donors

Under Section 0G, donors are exempted if a company registered under Section GG is registered.

Required Documents

- PAN card of all members

- All Members Aadhaar Card

- Latest bank statement of all members and company

- Telephone bill / Electricity bill

- Voter ID

- Passport

- Driving License

- Passport size photo of all members

- Copy of rental agreement

Appointment of Directors in Section 8 company

at least 3 & amp; Serially 2 directors and maximum 15 directors for a public limited and private limited company. However, there is no minimum or maximum prescription for Section 8 companies.

Guides a female director in a specified class of companies.

Each company commands a resident director.

While directing the total number of directors in Section 8 companies, the companies will not be presented briefly, that is, it shall not be added after the maximum limit of twenty directors as laid down in the Act.

Section 8 companies are not obliged to appoint an independent director and are exempt from all necessary provisions including autoregire directors.

Section 8 company requires the minimum requirement of a resident director, i.e. a leader who resides in India for a period of at least 182 days (one hundred and thirty-eight days) or more in the preceding table.

- Section 149 (1) of the 'Companies Act 2013'

- Second provision for section 189 (1)

- Section 149 (3) of the Companies Act 2013

- Section 165 of the Companies Act, 2013

- Section 149 (1) of ‘ Companies Act, 2013 ’

- Under Section 149 (3)

Eligibility Criteria

- An individual or HUF or limited company is eligible to initiate a Section-8 company registration within India.

- Two or more persons who will act as shareholders or directors of the company must satisfy all the conditions of section 8 company registration.

- At least one director will be a resident of India.

- The intention should be progress of sports, social welfare, advancement of science and arts, education and financial support to low-income societies.

- The surplus created should only be used to reach the prime objective of the Section 8 company.

- No member of the company can attract any kind of cash or any kind of compensation.

- No profit should be shared directly or indirectly between the association members and the director

- The company should have a different vision and framework plan for the next three years.

- Asset Management: The ownership of property is vested in the name of the company, and it can be sold only as per the rules mentioned under the Companies Act. (Ex: with the consent of the Board of Directors as a resolution).

- To meet the required compliance, accounts, reports and returns of the association with the ROC are required.

CSR Committy

- CSR Committee

The CSR committee of the board should cover the entire process by giving an artistic look to the CSR policy, listing the actions to be followed by the company. It should make a reference to the board on the budget set for the research of events. Based on the recommendations, the board will approve spending on each activity stated in the CSR policy. The CSR organization is vested with the obligation to monitor and control the implementation of the CSR policy. The money allocated for the projects should only be spent on the declared target.

- CSR Activities

The CSR committee is entitled to make a reference to the board on the exercises to be adopted under the CSR, on the basis of which, the board will conclude the CSR strategy. Some of the key aspects that come with CSR activities are:

1. CSR project should not be associated with daily business operations.

2. The Business (Corporate Social Responsibility Policy) Act, 2014, allows an arrangement for carrying out CSR activities through a Certified Trust / Certified Society / Section 8 company.

3. CSR organization should set up a monitoring and recording system to use the repository for CSR practice.

4. The company is also given an opportunity to collaborate with other companies which helps CSR committees of many companies to report independently on such projects or programs.

5. CSR movement of Indian reality should be in India only.

- CSR Spend

1. Bills spent outside of India on projects as per CSR policy will not be a component of CSR investment.

2. Cost on labor benefits will not be considered as CSR investment.

3. CSR expenses, including expenses incurred by the company on administrative overheads to its employees, and employees of performing agencies with a three-year track record, CSR expenses will be considered subject to the satisfaction of certain conditions.

4. Expenses incurred on payments to political parties will not come under the purview of CSR spending.

5. One-time programs such as marathons, awards, charitable contributions, advertisements, sponsorship of television programs etc. will not qualify as CSR expenses.

6. Remuneration paid to regular CSR employees as well as company volunteers for CSR activities can be paid as part of CSR expenses in CSR project costs.

7. Expenses earned by a foreign holding company for CSR activities in India will qualify as CSR expenditure of an Indian subsidiary, if CSR expenses are routed through Indian subsidiaries and if the Indian Subsidiary Act According to this it is necessary to do so.

Prospectus

As per the exception notification read with Sections 173 (1) and 174 (1), Section 8 companies must possess at least one meeting within six calendar months, and an integer eight for its board meetings. . The director or 1 / 4th are its total concentration, whichever is lower, sequentially. However, there should be a minimum of two members in attendance.

80G Certificate

The 80G certificate is awarded to a Section 8 company by a non-profit organization or non-governmental organizations (NGO), a 'charitable' trust or 'income tax department'. The purpose behind the 80G certificate is to give more donations to donors for such organizations. The main benefit is that the donor benefits from donating to such NGO that he gets tax exemption on 50% of his donation as the donor is allowed to deduct the donation from his gross total income.

12A registration

Significantly, 12A NGO registration, trust and NGO and other section 8 companies are exempted from income tax on employment. NGOs are primarily organizations that are created for charitable and non-profit purposes. However, they have revenue and if not registered under Section 12A of the Income Tax Act will have to pay a fee as per standard rates.

Annual Docility for Section 8 companies per the Companies Act 2013

GST Registration

PVT. LTD. Company

Loan

Insurance